In the very short time I have been working with the organization, I have come to admire RIMANSI as the microinsurance technical resource centre that several MBAs have endeavoured to establish.

What’s RIMANSI?

RIMANSI is short form for RIsk MANagement Solutions Incorporated. In 2005, a group of 8 organizations, consisting of co-operative MFIs, a local bank and a co-operative MBA, got together to establish an entity that would promote the MBA model as an effective and sustainable approach to the business of microinsurance and serve as a resource centre for MBAs:

- Alalay sa Kaunlaran, Inc. = MFI;

- Kasangyangan Foundation, Inc. = MFI;

- People’s Alternative Livelihood of Sorsogon, Inc. = MFI;

- Rural Bank of Talisayan = local bank in the rural town of Talisayan;

- USWAG Development Foundation = MFI;

- CARD MBA = MBA;

- CARD BANK = MFI; and

- CARD NGO = MFI.

The primary goal for establishing RIMANSI was to have an organization that would promote microinsurance on a larger scale using the delivery and collection systems used by various MFIs operating in rural or urban centres in different regions of the Philippines. [For those of you in Canada, picture “credit unions” when you think of MFIs.]

What does RIMANSI do?

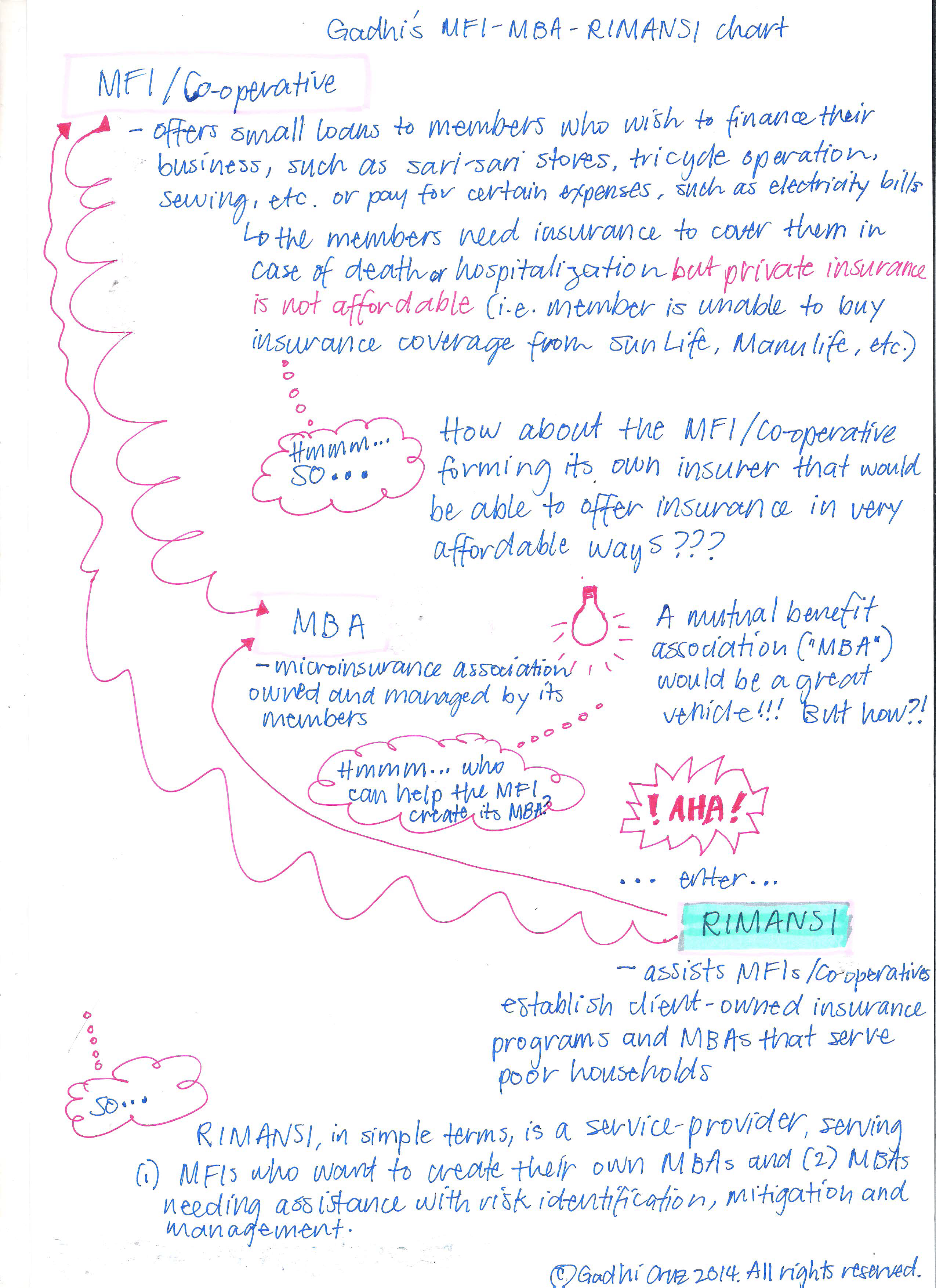

It took me a while to understand what exactly RIMANSI does, and even in my third week on the job, I was finding it challenging to understand its role in relation to MFIs and MBAs so I drew myself a chart, which I’m sharing with you in the hope that it would help you see what I’ve been describing above.

RIMANSI would achieve the goal of promoting the MBA approach to the business of microinsurance by helping each MFI create its own MBA. The MBA would serve as the MFI’s arm for promoting and selling microinsurance to poor people.

If you’re still confused at this point after seeing my chart above, don’t worry. I’m still confused too as they do a lot of other things besides setting up new MBAs for MFIs. We can be confused together! 😛

But, wait!!! Don’t give up too easily and don’t take the easy road of not reading further than this sentence!!! Bear with me… I will explain the MBA model that RIMANSI is trying to promote by crafting a fictional story in bullet form. 🙂

- There’s a poor person who has no work or livelihood–let’s call her Nanay Teresita [remember… nanay means mother].

- Nanay Teresita’s husband is a tricycle driver who earns less than P200 per day ($5 in Canadian currency)–let’s call her husband, Tatay Arturo [tatay means father].

- Nanay Teresita and Tatay Arturo have two kids, both of which are under 10 years old.

- Nanay Teresita wants to work or earn some money so she could help Tatay Arturo feed the family and perhaps send the kids to school.

- Nanay Teresita’s only skill is sewing–she could sew curtains for a living.

- There’s one problem: Nanay Teresita does not have a sewing machine–she will need to buy one if she were to sew for a living. She and Tatay Arturo do not have the money to buy one. What to do, what to do???

- Luckily for Nanay Teresita, there’s an entity that lends money to poor people (at a very low interest rate and affordable weekly payments) who want to establish a small business. This entity is referred to as a “microfinance institution” (MFI)–let’s call the MFI in this story, Co-op Bank.

- Co-op Bank would be willing to lend Nanay Teresita some money so she could buy a sewing machine and start earning for the family, but with conditions. Nanay Teresita has to become a member of Co-op Bank to get the loan and must attend a weekly “centre visit” to see a loans officer. During the weekly meeting with the loans officer, Nanay Teresita would have to provide the loans officer with her loan payment and a quick update on her business. Nanay Teresita would be referred to Co-op MBA to obtain basic life insurance. Co-op Bank loans officer would collect Nanay Teresita’s insurance premium from her during the weekly centre visit and remit the premium to Co-op MBA immediately.

- Nanay Teresita agrees with Co-op Bank’s terms and conditions. She now has the capital to start her business–she can buy herself a sewing machine and start sewing curtains! In addition, she was able to get life insurance through Co-op Bank, which would help her and her family in case of death or illness. Yay!

- Where does RIMANSI come in??? Co-op Bank is a small financial institution owned by members. Although Co-op Bank has a ton of members who need basic life insurance coverage, it is unable to service this need because it has no channel for selling insurance. Co-op Bank would need to set up this channel, a mutual benefit association (MBA), that would sell life insurance to poor people, like Nanay Teresita. Co-op Bank connects with RIMANSI to get help on setting up its microinsurance arm called, Co-op MBA. RIMANSI does its magic and soon enough, Co-op MBA is established.

Members of MFIs would automatically be referred to the MFIs’ respective MBAs to obtain microinsurance products, such as basic life insurance or, if the MBA offers it, credit life insurance. Basic life insurance coverage would typically include death benefits and coverage for funeral and hospitalization.

To give you an additional visual idea of what microinsurance and RIMANSI are about, I encourage you to see the video below.

Video

The song on the video’s background, is called “Kaagapay” and was written by Mimo Perez.

Song

Mimo has provided the following context behind the song:

The Filipino word, “kaagapay“, is an inclusive word that signifies companionship, guidance and assistance. In kaagapay, there is a hint of respect on the side of the helper for the helpee’s quest for self-determination. Beyond RIMANSI’s engaged solidarity with the poor, being kaagapay boils down to the organization’s desire to empower the poor to help themselves. Kaagapay in this sense, captures the spirit and the organizational thrust of RIMANSI.

Like any jingle, but without compromising the core message, the lyrics and music of Kaagapay were intentionally made simple and catchy for easy recall and instant participation of the assembly.

© Mimo Perez 2014. All rights reserved.

RIMANSI has achieved a lot since its inception in 2005 as the figures below show:

- in 2007, the MBAs that RIMANSI helped set up had a membership count of 518,274; in 2013, the membership count was at 2,370,048.

- in 2007, the MBAs collected a total of P247,109,783.04 in insurance premium ($6,177,745 CDN); in 2013, the total insurance premium collected was P1,455,109,334.80 ($36,377,733 CDN).

- in 2007, the MBAs paid P40,406,369.02 in claims ($1,010,159 CDN); in 2013, they paid P361,198,774.53 in claims ($9,029,969 CDN).

- RIMANSI services 14 MBAs currently.

Aside from setting up new MBAs for MFIs and enabling 20 community-based organizations to provide insurance to their members in 6 years, RIMANSI has:

- made micro-insurance accessible to the poor and help them empower themselves to own and govern their micro-insurance programs;

- helped establish the legal framework for microinsurance in Asia and the Pacific, especially in the Philippines; and

- established performance standards for MBAs to push them towards self-regulation and sustainability.

RIMANSI visited one of The Co-operator’s subsidiaries, The CUMIS Group Limited, in Burlington, Ontario, Canada in 2011. Craig Marshall, Vice President and General Counsel for The Co-operators’ life insurance operations, who was part of the hosting team, said the following to me about RIMANSI:

That organization is like CUMIS in a time machine in the early days. Very exciting and good work that they do. We hosted them in February, 2011 with their CEO at the time, Epifanio A. Maniebo and an actuary, Mae Lungayl. My colleagues Rudy Capogna and Dirk Sack were struck by how similar it was to CUMIS in the early days of the credit union movement of the late 30′s and early 40′s.

Front Row (left to right): Mr. Derek Cameron (CCA Program Officer), Ms. Mae Elizabeth Lungay (RIMANSI actuary) and Mr. Epifanio A. Maniebo – Chief Executive Officer of RIMANSI. Back Row: Craig Marshall (Vice President, General Counsel – Life Operations and Secretary) Rudy Capogna (Vice President, Property and Casualty Insurance) and Dirk Sack (Vice President, Creditor Insurance).

For an organization this young (9 years old!!!), RIMANSI has done quite a lot and has received recognition and respect from the Insurance Commission, the insurance regulator of the Philippines. If it’s true that RIMANSI’s trajectory mirrors that of CUMIS’ in the late 30′s and early 40′s, and the current CUMIS is where RIMANSI is headed, then RIMANSI’s future is looking so bright, it can light up the dark Philippine sky!

The MBA model being promoted and championed by RIMANSI is just the beginning of a beautiful thing.

Gadhi, what a great and easy to read explanation! Thanks for posting! 🙂 I didn’t know that RIMANSI has only been around for 9 years – they’ve done great things!